The Indian School of Business (ISB) is a premier business school in India, renowned for its world-class MBA programs, global faculty, and strong industry connections. It comes under the 50 best business schools in the world. Of course, it is the number one business school in India. A person with a PhD from a reputed institution and exceptional research and teaching skills, joins here as a professor and has published several high-quality research papers in the Financial Times list of top 50 journals worldwide. This is why ISB is ranked as India’s best business school. In the history of its last 22 years, there has been only one professor in the finance department. Prof. Prasanna Tantri from ISB Hyderabad, who without company, had taken only two years to achieve the tenure. Prof. Prasanna Tantri is a distinguished faculty member at the Indian School of Business (ISB) in Hyderabad. He is a respected scholar known for his expertise in finance and economics. He is also the executive director of Analytical Finance and independent director of Power Finance Corporation.

Table of Contents

Journey from village to insurance agent & ISB

Prof. Prasanna Tantri is from Udupi, a coastal town in the south-western state of Karnataka, India. Bankerkatta is a village in Udupi, where he spent his childhood. His father was a Hindi teacher. He started his education in a Govt. school. For his higher education, he went to Manipal, not far from Udupi. In his younger days, he wanted to be a politician as he had more close interactions with a lot of people in RSS (Rashtriya Swayamsevak Sangh). He observed that a lot of powerful people lived simply and had a big impact on societies. He explains that maybe he could have got inspired by them during his younger days. Then he got interested in economics and ended up joining commerce. In fact, when he went for 11th-standard admission he had to convince of his interest in commerce to the principal because during those times students with higher scores used to select science. It even took him years to recognize what he really liked in economics and then he came to ISB. There was a lot of struggle before he landed in academic research.

He landed in ISB after clearing the GMAT exams. He was married at that time and got support from his family too. After reaching here he found that professors and people doing research in a way of sitting and thinking and writing papers. From there he understands and chooses academic research. But the intention was not about research by joining ISB, he thought of doing something in insurance and doing MBA. Eventually, he started interacting with the top quality researchers and started reading more. Afterwards, he got a job at ISB and did his PhD. Now, he is a faculty member there.

After his B.com, he started his first job. During that period his father was retiring from teaching and he was working on different courses, without knowing what to do. Finally he came to the decision to take up a sales job. His friend Kishan helped him to find this job as he did not have any proper experience. ICICI Prudential Company was the first company he worked for. His job was to mentor insurance agents, train them to sell policies and meet targets.

Understanding the impact of government spending on our economy is crucial. In our discussion with Dr. Prasanna Tantri, we delve into the intricacies of government expenditure, highlighting its potential to drive economic growth, as well as the risks of inefficiency and corruption. This comprehensive look at the good, bad, and ugly sides of government spending sheds light on its complex effects on society and the economy. For those interested in the mechanisms that shape our financial world, this exploration is indispensable.

How to make money from boring businesses?

In general, equity is the ownership interest in an asset or company, and insurance is a contract that provides financial protection against specific risks.

If you are referring to insurance in the context of investments, there are insurance products such as equity-indexed annuities that link returns to the performance of stock market indexes, but these are not commonly referred to as “equity insurance.” Prof. Prasanna Tantri was told that money doubles in equity in three years during his initial days of job. There was a time when the market was booming, like from 2003 to 2009, India grew at 8 and ups. So it is true that money doubled in 3 years. This sold a lot of insurance and it was the beginning of private insurance in India. Then he used equity insurance and eventually his middle-class fears triggered and he would suggest his clients to allocate a lot of money to bonds. After reading the US market history he knew that this was not going to last forever. For a normal person, passive investing is the best thing to index investment. Even now there are people being misled, about past performances.

Peter Lynch, a legendary fund manager and author known for his success with the Fidelity Magellan Fund, often emphasized the idea that investment is a combination of art, science, and legwork. Let’s break down what he meant by this statement:

- Art: The “art” aspect of investment refers to the subjective and creative elements involved in making investment decisions. It includes factors like intuition, judgment, and an understanding of market psychology. Successful investors often have a knack for spotting trends or opportunities that may not be immediately obvious from quantitative data alone. This intuitive aspect of investing is what sets some investors apart from others.

- Science: The “science” aspect of investment refers to the quantitative and analytical aspects of the process. It involves analyzing financial statements, studying economic indicators, and using various financial models to assess the potential risks and returns of an investment. This scientific approach provides a foundation for making informed decisions based on data and evidence.

- Legwork: The “legwork” aspect of investment highlights the importance of thorough research and due diligence. Successful investors typically spend a significant amount of time researching companies, industries, and market conditions. This may involve reading annual reports, attending shareholder meetings, speaking with industry experts, and staying updated on news and developments that could impact their investments. Doing the necessary legwork helps investors make well-informed decisions and reduces the element of surprise.

In essence, Lynch’s statement underscores that successful investing is a multifaceted endeavor. It’s not just about crunching numbers or relying solely on intuition; it’s a holistic approach that combines both qualitative and quantitative analysis with diligent research and a keen understanding of market dynamics. By acknowledging the art, science, and legwork aspects of investment, Lynch emphasizes that successful investors must be well-rounded and adaptable in their approach to navigating the complex world of finance.

There is also the statement “Invest in people, not in business” which underscores the idea that the success of a business often hinges on the people behind it, such as the founders, employees, and leadership team. Here’s an explanation of this concept:

- Talent and Expertise: People bring their skills, expertise, and talents to a business. Investing in individuals with the right skills and experience can be more important than the business idea itself. A talented and motivated team can adapt to changing circumstances, innovate, and overcome challenges effectively.

- Leadership and Vision: Strong and capable leadership is essential for a business’s long-term success. When you invest in people who have a clear vision, strategic thinking, and the ability to lead and inspire others, you are more likely to see the business thrive and grow.

- Innovation and Adaptability: People are responsible for driving innovation within a business. They come up with new ideas, adapt to market changes, and find creative solutions to problems. Investing in individuals who possess these qualities can lead to a business staying competitive and relevant.

- Company Culture: The culture of a business is often shaped by its people. Investing in individuals who align with the company’s values and culture can lead to a positive work environment, increased employee satisfaction, and better overall performance.

- Resilience and Problem-Solving: Businesses inevitably face challenges and setbacks. People who are resilient and adept at problem-solving can help a business weather difficult times and emerge stronger.

- Customer Relationships: People are also responsible for building and maintaining relationships with customers and clients. A strong customer-focused team can drive customer loyalty and business growth.

- Long-Term Success: While a business idea may be innovative and promising, its success is often determined by how well it is executed. Talented and committed individuals can turn a mediocre idea into a successful business through their dedication and hard work.

Thus investing in people means recognizing that the individuals who make up a business are its most valuable assets. Their skills, dedication, and ability to work together effectively can ultimately determine the success or failure of the business. While a good business idea is important, it’s the people behind it who bring that idea to life and drive it toward long-term success.

“One Up On Wall Street” by Peter Lynch is a classic book on investing that provides valuable insights into Lynch’s investment philosophy and strategies. Lynch is a legendary fund manager known for his successful tenure at Fidelity Magellan Fund, and in this book, he shares his wisdom with investors. One of the key principles discussed in the book is the idea that ordinary individuals can achieve success in the stock market by applying common sense and paying attention to their everyday experiences.

Example: The Coffin Business:

Lynch uses a memorable example involving the coffin business to illustrate his investment philosophy. He explains that sometimes the best investment opportunities are right in front of us, in our day-to-day experiences.

In the book, Lynch describes a situation where he noticed that his wife’s friends were discussing the growth of a small, local company that produced high-quality coffins. He did some research and realized that this company, which wasn’t well-known on Wall Street, had a solid niche market and a unique product offering.

Key Takeaways from the Coffin Business Example:

- Pay Attention to What You Know: Lynch emphasizes the importance of investing in businesses or industries you understand. In his case, he understood the coffin business because he had heard about it from people he knew.

- Small Can Be Profitable: Lynch’s investment philosophy includes looking at small, lesser-known companies that may not attract much attention from professional analysts or institutional investors. These companies can sometimes offer substantial growth potential.

- Long-Term Perspective: Lynch’s approach is rooted in a long-term perspective. He didn’t buy the coffin company’s stock expecting overnight success. Instead, he recognized its potential for steady growth over time.

- Contrarian Thinking: Lynch’s willingness to invest in an unconventional industry like coffins exemplifies his contrarian thinking. He wasn’t swayed by popular trends or fads but focused on the fundamentals of the business.

- Research and Due Diligence: Lynch didn’t blindly invest based on hearsay. He conducted thorough research to understand the company’s financials, competitive position, and growth prospects.

“One Up On Wall Street” by Peter Lynch is not just a book about investing; it’s a guide to thinking differently about investing. Lynch’s approach emphasizes the importance of common sense, research, and paying attention to everyday experiences to identify promising investment opportunities. The example of the coffin business illustrates how Lynch’s philosophy can lead to successful investments in unexpected places. Investors can benefit from Lynch’s practical wisdom and his belief that with the right approach, anyone can achieve success in the stock market.

As we navigate through our financial journeys, planning for retirement emerges as a paramount concern. Dr. Pattabiraman’s talk offers invaluable advice on crafting a robust retirement plan that secures your future. Delving into effective strategies and common pitfalls, this conversation is a treasure trove of wisdom for anyone looking to ensure financial stability in their golden years. Whether you’re just starting your career or nearing retirement, these insights can guide you towards a comfortable and secure retirement.

Can machine learning replace loan officers?

What is machine learning?

In simple terms, Machine Learning is a subfield of artificial intelligence (AI) that focuses on the development of algorithms and statistical models that enable computers to improve their performance on a specific task through learning from data, without being explicitly programmed. In essence, machine learning allows machines to recognize patterns, make predictions, and adapt their behavior based on the information they are exposed to.

It cannot fully replace loan officers, prof says that it can definitely assist them. For a loan, there are two pieces of information:

- Hard information: height, weight, etc. which is for verification.

- Soft information: this means whether the person is innocent, his behavior, truthfulness, integrity, etc.

For these machine learning won’t help, it needs officers. If both are combined, machine learning and human, it can get a good result. The main point is that we will be able to get a biased result, and there won’t be any discrimination.

How does academic research impact the common man?

There are many ways that academic research is getting involved in common man. In this Prof. Prasanna Tantri is mainly sticking to the topics “economics and finance”.

- The first is policies:

Every policy has an intellectual radar. The intellectual framework for monetary policy comes from academic research.

- Regulations in the policies:

- How much disclosure should companies make?

- What is optimal and not optimal?

These questions eventually infer the policies.

- Academic research papers are used as study materials in universities.

Example:

- How to value a stock?

- Credit rating.

Prof. Prasanna Tantri explained the opportunity that he had got to discuss the topic “if you remove people from a tax audit, tax compliance goes up” with the finance minister in the pre-budget meeting. His other paper on the topic, Loan Officers is used as a textbook in a university for teaching. He also includes that research is about the present, which has diagnoses and predictions.

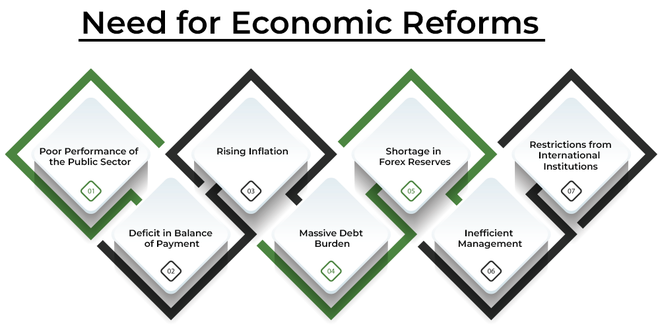

Tax reforms that India needs

In India, this new tax structure is good for people, but may not be good for the country. In 2007 the country’s savings rate was 38%, now it is 29%. This shows that the savings rate is falling.

The saving rate, also known as the savings rate, is a financial metric that measures the percentage of income that an individual or a household saves rather than spends on consumption. It reflects the portion of income that is set aside for future use or investment, rather than being immediately spent on goods and services.

Example:

Suppose Raj, an individual in India, earns a monthly income of 10,000 Indian Rupees (INR). Over the course of a month, he decides to save 2,000 INR and spends the rest on various expenses.

To calculate Raj’s saving rate, you can use the formula:

Savings Rate (SR) = (Income after-tax – spending) / (Income after tax)

So, Raj’s saving rate is 20%. This means that he saves 20% of his monthly income (2,000 INR) and spends the remaining 80% (8,000 INR) on his monthly expenses. A higher saving rate indicates a greater portion of income being saved for future needs or investments, while a lower saving rate suggests more income is being used for immediate spending.

Investment always facilitates growth. In the long term there are only two ways you can increase growth:

- By investing

- By improving technology (more productivity).

Thus it is recommended that more policies encourage savings not conceptions. Conceptions are for short-term money making.

In our pursuit of financial security, being well-informed about the nuances of pension schemes is essential. Our detailed look into the hidden pension rule unveils critical aspects that could significantly impact your retirement planning. Understanding these rules ensures that you can navigate the complexities of pension schemes effectively, maximizing your benefits and avoiding potential pitfalls. This knowledge is crucial for anyone looking to optimize their retirement savings and ensure a steady income in their later years.

Government covid action plan critique

The govt has given food through PM Garib Kalyan Anna Yojana. It was a direct conception and along with that cash was also given to the people. Instead of converting all the money to food and other needs, people have saved half of it. There is evidence that shows this. About 20,0000 crores have been transferred to PMGKAY by the govt, but it was not used by the people. During a crisis people are worried and it is not a good platform for focusing on conceptions. It was a great strategy. Also, the govt has not given any loans, they have provided Grandy more than loans. Because banks were reluctant to lend. In ECLGS, through this scheme, the Indian government aims to provide Rs. 3 lakh crore of unsecured loans to MSMEs (medium and small enterprises) and companies across the country. This is to mitigate the losses suffered due to COVID-19-induced lockdowns. It is a business loan in which 20% of grandy is given by the govt. agencies. This made many small businesses pay their rent, and pay their employees during that time. This was a temporary relief for most of them. After the crisis period, most of the funds were withdrawn. Prof. Prasanna Tantri supports what the govt has done during the crisis period, but not with continuing with the schemes now.

Mudra loan a flop?

Prof. Prasanna Tantri disagrees with the govt regarding this, as these are short-term fixes. In Mudra, people don’t know about the true default rate. Credit cannot be forced, credit should build an infrastructure that can be used for machine lending.

Example: SBI has more information and data. They are willing to lend money to small people. SBI LIFE a private company, creates SBI FIN TECH a separate company that uses SBI’s data and uses machine lending. This creates a competition and that leads to better learning practices.

Now in India, there is a scheme called SVANidhi to provide handholding support to street vendors, Ministry of Housing and Urban Affairs (MoHUA) launched PM SVANidhi a micro-credit scheme, facilitating a working capital collateral-free loan of ₹10,000, with subsequent loans of ₹20,000 and ₹50,000 with 7% interest subsidy. The ultimate aim of this scheme is for people to borrow in the normal credit market

Are Government decisions rational?

In the budget, there are two initiatives:

- Self-help groups:

Self-help groups (SHGs) play a significant role in economic development and empowerment in India. These groups are typically formed by a small number of individuals, often women, with a common goal of improving their socio-economic conditions. SHGs focus on savings, credit, and various income-generating activities. Here are some key aspects of self-help groups in the Indian economic context:

1. Savings and Credit:

SHGs encourage members to save regularly, even small amounts, which are then collectively used for providing loans to group members.

Members can borrow from the group for various purposes, including starting or expanding small businesses, covering health expenses, or meeting household needs.

Interest rates on loans from SHGs are usually lower than those from traditional moneylenders, which can help members break free from the cycle of high-interest debt.

2. Income Generation:

SHGs often engage in income-generating activities, such as small-scale agriculture, handicrafts, tailoring, and micro-enterprises.

These activities help members supplement their household income and improve their economic status.

3. Skill Development:

SHGs may provide training and skill development programs to members, enhancing their capacity to engage in income-generating activities successfully.

4. Empowerment:

SHGs empower individuals, especially women, by providing them with a platform to voice their concerns and make decisions collectively.

Members gain confidence, financial literacy, and leadership skills through participation in SHGs.

5. Government Support:

The Indian government has recognized the importance of SHGs in poverty alleviation and women’s empowerment and provides financial support and subsidies to promote their formation and growth.

Several government schemes, such as the National Rural Livelihood Mission (NRLM) and the Deen Dayal Antyodaya Yojana-National Rural Livelihoods Mission (DAY-NRLM), focus on strengthening SHGs in rural areas.

6. Microfinance Institutions (MFIs):

Some SHGs collaborate with microfinance institutions (MFIs) to access larger loans for their members, enabling them to undertake more significant income-generating activities.

7. Social Development:

In addition to economic benefits, SHGs often contribute to social development by addressing issues like health, sanitation, and education within their communities.

8. Challenges:

Despite their positive impact, SHGs face challenges such as ensuring financial sustainability, building capacity, and adapting to changing economic conditions.

Self-help groups have become a valuable tool for economic empowerment and poverty reduction, particularly in rural India. They foster financial inclusion, women’s empowerment, and community development while providing individuals with the means to improve their economic well-being. The self-help groups are lent from many private banks to start their work or else the govt helps them in funding.

Lending and facilitating lending are pivotal components of any nation’s economic infrastructure. Access to credit is essential for individuals and businesses to pursue opportunities, invest, and foster economic growth. Governments often play a crucial role in shaping lending policies and creating an environment conducive to both borrowers and lenders. Lending is the process of providing financial resources, typically in the form of loans, to individuals, businesses, or governments. It serves as the lifeblood of economic growth and development. In a well-functioning economy, lenders (such as banks, financial institutions, and even peer-to-peer platforms) provide capital to borrowers, enabling them to invest in productive ventures, purchase homes, educate themselves, and meet unforeseen expenses.

Governments play a multifaceted role in facilitating lending within an economy. This role includes:

- Regulation and Oversight: Governments enact and enforce laws and regulations that govern lending practices to ensure fairness, transparency, and consumer protection. This oversight aims to prevent predatory lending and maintain the stability of the financial sector.

- Monetary Policy: Central banks, which are often government entities, influence lending through monetary policy. By adjusting interest rates and implementing open market operations, they can stimulate or cool down lending activities, depending on the economic context.

- Financial Inclusion: Governments strive to promote financial inclusion by making credit accessible to marginalized or underserved populations. They may establish initiatives or institutions dedicated to providing affordable loans to these groups.

- Credit Guarantees: In times of economic distress or uncertainty, governments may offer credit guarantees to encourage lending by reducing lenders’ risk exposure. Such measures aim to keep credit flowing, even during crises.

- Incentives for Lenders: Governments can incentivize lending by offering tax breaks or subsidies to financial institutions that provide credit to specific sectors or regions, thus fostering economic development.

The rationality of government decisions regarding lending and facilitating lending is a subject of debate, as it depends on various factors:

- Economic Context: Government decisions must be adaptable to the economic situation. What is rational during a recession might not be during a boom. Governments must strike a balance between stimulating lending during downturns and preventing reckless lending during upswings.

- Political Influence: Political considerations can sometimes cloud rational economic decisions. Pressure from interest groups, lobbying, or electoral considerations may lead to sub-optimal lending policies.

- Long-Term vs. Short-Term Goals: Governments may prioritize short-term political gains over long-term economic stability. For instance, offering excessive credit guarantees without proper risk assessment can lead to fiscal challenges in the future.

- Unintended Consequences: Government interventions can sometimes have unintended consequences. Policies that promote lending to certain sectors may result in asset bubbles or financial instability.

- Transparency and Accountability: The rationality of government decisions also hinges on transparency and accountability. Policies must be well-documented, debated, and evaluated over time to ensure their effectiveness.

Lending and facilitating lending are vital cogs in the wheel of economic progress. Government decisions in this domain carry significant implications for a nation’s economic well-being. The rationality of these decisions depends on various factors, including economic context, political influences, and the pursuit of both short-term and long-term goals. Rational government decisions in lending should prioritize economic stability, fairness, and the welfare of all citizens, ultimately promoting sustainable economic growth. Therefore, policymakers must carefully weigh the pros and cons of their choices and engage in continuous evaluation to ensure that lending policies remain rational and responsive to changing circumstances.

Coming to group loans and individual loans, many studies have shown that after the crisis people have mainly paid their group loans rather than that of individual loans. Govt should facilitate credit infrastructure rather than lend on its own. Being in the community is the main thing.

Harmful effects of Government policies

Policy restructuring that may have occurred in 2008 related to non-performing (NP) loans or assets by banks. The year 2008 was a significant period in the global financial industry due to the financial crisis that began in the United States and had ripple effects worldwide. During this time, many banks faced challenges related to NP loans and had to restructure their policies and operations to address the crisis. Even after the crisis period, the economic growth was 9.7% in 2009. This shows that the policy restructure was not reversed after the crisis. Thus the banks started lending money instead of supporting the needy because NP recognition was not there. Here the govt had to withdraw this act as soon as the crisis was over. Instead of this, the credit grows up to 30%. Other than saving institutions in distress it became free for all. In 2013 and 2014 India had the worst economy, because of these reasons.

Raghuram Rajan’s bank plan – masterstroke or blunder?

Raghuram Rajan is a prominent economist and former Governor of the Reserve Bank of India (RBI). His tenure at the RBI, from 2013 to 2016, was marked by several policy initiatives and reforms. One of his notable plans was the introduction of the Asset Quality Review (AQR) in 2015, which aimed to address the issue of non-performing assets (NPAs) in Indian banks. Supporters argue that it was a necessary step to address the NPA crisis and bring transparency to the banking sector, while critics suggest that it may have had unintended negative consequences, particularly in the short term. The long-term impact and effectiveness of the AQR in stabilizing the Indian banking sector remain the subject of ongoing debate. The Asset Quality Review (AQR) is a comprehensive assessment process used by central banks and regulatory authorities to evaluate the quality of a bank’s assets, particularly its loan portfolio. The primary objective of an AQR is to ensure transparency and accuracy in the reporting of a bank’s non-performing assets (NPAs) and assess its financial health accurately.

RBI has done an audit to find the true level of bad laws. For this, they first withdrew the forbearance, then RBI went into each and every large role. Thus RBI discovered true NP’s at bank is not actually 2%, but 11%. The problem here was that the RBI was also at fault at that moment. Another problem found here is that the RBI imagined that the govt would recapitalize immediately. Here the RBI and govt both were not working in coordination. In 2018 and 2019 they mobilized resources and capitalized. Now banks are in the best shape. The core of the problem was forbearance and the way they handled it was also a problem.

How the bankruptcy code helped banking

The bankruptcy code, also known as the insolvency and bankruptcy code (IBC) in India, has had a significant positive impact on the banking sector in India. Enacted in 2016, the IBC was designed to streamline and expedite the resolution process for insolvent or stressed companies. Here’s how the bankruptcy code has helped the banking sector:

- Timely Resolution of Bad Loans: Prior to the IBC, the process of resolving bad loans in India was protracted and cumbersome. The IBC introduced a time-bound resolution process, which has helped banks recover their dues more efficiently. This has had a direct impact on reducing the burden of non-performing assets (NPAs) on banks’ balance sheets.

- Increased Recovery Rates: The IBC has improved recovery rates for banks. Under the code, creditors have a say in the resolution process, and the assets of the insolvent company can be sold or transferred to a new buyer, thereby maximizing the value of these assets. This has allowed banks to recover a higher percentage of their outstanding loans.

- Professional Insolvency Professionals: The IBC introduced the concept of insolvency professionals who oversee the resolution process. These professionals bring expertise and objectivity to the process, ensuring that it is conducted efficiently and fairly. This has boosted confidence among creditors, including banks.

- Prevented Value Erosion: Under the earlier regime, the longer it took to resolve a distressed company, the more its value eroded. The IBC’s time-bound approach prevents such value erosion, preserving assets for creditors, including banks.

- Promotion of Responsible Lending: The IBC has encouraged banks to adopt more responsible lending practices. Knowing that there is now a more effective mechanism for resolving bad loans, banks have become more cautious about extending credit to borrowers with weak financials, thereby reducing the risk of future NPAs.

- Enhanced Credit Culture: The IBC has promoted a credit culture where borrowers understand that defaulting on loans can lead to swift and strict consequences. This has encouraged borrowers to make genuine efforts to repay their loans and resolve financial distress before it escalates.

- Reduced Litigation: Prior to the IBC, the resolution process was often marred by prolonged legal battles. The code encourages out-of-court settlements and provides a clear legal framework for resolution, reducing the need for extensive litigation.

- Improving the Health of Banks: As banks recover more of their dues and reduce NPAs, their financial health improves. This, in turn, strengthens the stability of the banking sector and enhances its ability to support economic growth through lending.

- Increased Investor Confidence: The IBC has improved investor confidence in the Indian banking sector. The efficient resolution of bad loans and stressed companies has made Indian assets more attractive to both domestic and foreign investors.

The bankruptcy code (IBC) in India has helped the banking sector by providing a more efficient and time-bound mechanism for resolving bad loans and stressed companies. It has led to higher recovery rates, improved the financial health of banks, and promoted responsible lending practices, ultimately contributing to the overall stability and growth of the banking sector and the Indian economy.

If a default case goes to IBC, the management will lose their job. First, it was the BIFR system. In this, if your number is negative then it will go under bankruptcy. And in bankruptcy, the owner is in charge. Thus the firms were using this strategically to run away from banks. After applying in BIFR the case will be read or the company will lose the company’s money and by the time of settlement, the company won’t have any money. This is what was happening in India untill 2016. Now IBC can take you to NCIT for default. First, the current board or the management will lose their job (company board). Then an administrator is appointed who will run the company. The lenders/ creditors will form a board and they will become the board and run the company. Thus preventive measures have a great impact.

How middle class can become rich?

Prof. Prasanna Tantri says that there is no short-term solution, ultimately increase in production or skill development is needed. The solution is to develop skills, we have to invest in our human capital. This means that people have to get out of the survival mindset to improve their human capacity and skills. The govt cannot do it, but govt can promote this. The responsibility lies within us. The spirit of entrepreneurship is within us. The govt has the potential to promote entrepreneurship among people of the country. The govt is good at promoting the private sector in credits and investments. So govt should facilitate the private sector rather than doing it all.

Why is India behind in manufacturing?

One of the govt advisors, Dr. Aravind, has diagnosed the problem with manufacturing in the way we started. In 1947, we had a 20% literacy rate and we focused on large-scale manufacturing, large-scale universities, large-scale technology, etc. 80% of the population was struggling during that period, so we had to start with the smaller items. Like toys, slippers, etc. This could have helped them as well. It could have been done in a way by taxing the import, but this could be a short term. Coming to a long-term system, we have to focus on diagnosing, finding the problems, etc.

The real reason behind brain drain

Brain drain refers to the emigration of highly skilled and educated individuals from one country to another, often resulting in a loss of talent and expertise for the source country. In the case of India, brain drain has been a long-standing concern. One of the primary reasons for the brain drain from India is the lure of better economic opportunities in developed countries. Highly skilled professionals, including engineers, doctors, scientists, and IT specialists, often find more lucrative job offers, higher salaries, and improved living standards abroad. Brain drain in India is a multifaceted issue driven by a combination of economic, educational, career-related, and personal factors. While it poses challenges in terms of talent loss, it also highlights the need for India to create an environment that attracts and retains skilled professionals, fosters innovation, and provides opportunities for career growth and personal fulfillment.

Prof. Prasanna Tantri believes that with time this could be naturally solved. The opportunities are getting a heads up. The world GDP rate is likely to grow by 2.5 trillion dollars, which means 400 billion will come from India itself. This proportion is only going to grow. A lot of entrepreneurial and research people will stay back in India, because of the growth itself.

SEBI, RBI, IRDAI vs Businesses

One of the regulations in India is far more challenging. This has both pros and cons. Theoretically, the banks are different because it is very difficult for a depositor to figure out the regulations in banks. In keeping trust in banks, it is necessary to detect the regulations.

Book recommendations by Prasanna Tantri

- “One Up On Wall Street” by Peter Lynch.

“One Up On Wall Street” emphasizes the significance of personal knowledge, study, and analysis in stock market trading, and it serves as a practical guide to effective investment techniques and philosophies.

- “Intelligent Investor” by Benjamin Graham.

The Intelligent Investor is a great book for beginners, especially since it’s been continually updated and revised since its original publication in 1949. It’s considered a must-have for new investors who are trying to figure out the basics of how the market works. The book is written with long-term investors in mind.

- Security Analysis by Benjamin Graham.

Security Analysis is essential to a proper understanding of investment fundamentals, as it has been since 1934.

- Journal of Economic Perspectives.

Check out the full podcast with Prof. Prasanna Tantri below:

{kind=link}